[ad_1]

[ad_1]

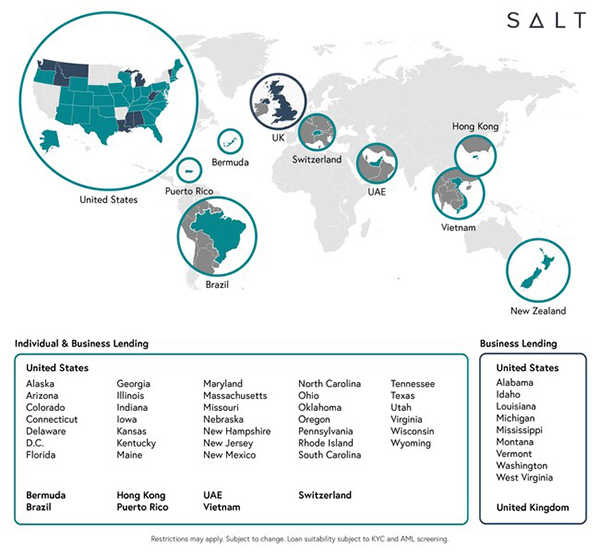

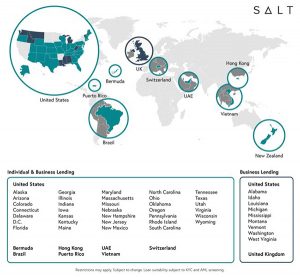

The SAL has recently undergone massive internal expansion and is now in 10 different countries. (PRNewsfoto / Salt Lending Holdings Inc.)

A former executive of a Denver-based cryptocurrency claims to initiate a recent court case that is being investigated by the Federal Securities and Exchange Commission.

And this is only the beginning of his complaints.

David Lechner sued Salt Lending Holdings Inc. at the Denver District Court last week, accusing the start of 2 years of unjust termination and at the same time claiming that executives covered the theft of millions of hackers in cryptocurrency, issuing loans self-service to the family and outpost in the Indian Ocean in a country that has relaxed financial regulations and no extradition agreement with the United States.

"The defendants have placed their personal interests above those of Salt, its members, its debtors and its shareholders," Lechner said in the lawsuit.

Jennifer Nealson, Salt's chief marketing officer, declined to comment on the specification of Lechner's claims.

"Although we have not yet had the opportunity to completely review the allegations made by the past employee, for political reasons we do not comment on issues related to employment," he said in a written response to BusinessDen.

Salt confirmed that the company was investigated by the SEC, according to a story in the Wall Street Journal.

"The SEC began investigating and suing many high-profile cryptocurrency companies that required information to better understand the industry and any potential need for additional regulations," Nealson wrote.

Colin Barnacle with Akerman is representing Lechner in the complaint. Barnacle and Lechner both refused to comment.

Plaintiff worked in Salt for less than a year

Salt, founded in 2016, provides its customers with encrypted cash loans. Nealson said the company, which has expanded its office presence on 17th Street in downtown Denver to 25,000 square feet at the start of this year, has about 70 employees.

David Lechner. (LinkedIn Headshot)

According to the lawsuit, Lechner started working in Salt in July 2017 as a "senior financial advisor". On her LinkedIn page, Lechner describes her role as chief financial officer.

Lechner's lawsuit challenges the company as a defendant and four current or former Salt executives: Shawn Owen, Gregory Bell, Benjamin Yablon, and Blake Cohen. Neither Yablon nor Cohen replied to BusinessDen's comment requests.

Lechner was put on administrative leave in April, according to the lawsuit. Nealson confirmed that in June 2018, Lechner no longer worked for the company.

A symbolic offering

Salt sold to the public $ 47 million in salt tokens through an initial coin offering launched in June 2017, according to the lawsuit. Companies that create a cryptocurrency launch an initial money offer, similar to an IPO, for investors who buy new currencies.

Lechner argues that it was his refusal to return the salt tokens that led to his resolution. In April and May, Cohen, Owen, and Bell asked Lechner to return his salt tokens, the same form of cryptocurrency as the company Lechner had received as part of his first employment contract. In July, Lechner's salt tokens were valued at $ 12.1 million, according to the lawsuit.

The lawsuit alleges that Salt prevented Lechner from redeeming his tokens in cash. The balance that Lechner eventually recovered was about $ 300,000, according to the lawsuit.

SALT provides its customers with encrypted cash loans. (Screen image)

In February, Salt and a related entity, Salt Blockchain Asset Management, received quotes from the SEC, according to the lawsuit.

"Salt is currently the subject of a quote and an investigation by the SEC regarding its non-registration of salt tokens as" titles "and other related issues," says the lawsuit.

The SEC declined to comment.

Suit: Failure to change Exec's password resulted in massive theft

In October 2017, according to the lawsuit, a hacker got access to the Salt & # 39; s Mailchimp account and captured 60,000 email addresses and personal information from Salt members, as well as e-mails containing information such as password resets.

The lawsuit said that Bell never reset his password Slack after hacking, and it is believed that the original attacker monitored the account for months, then performed a "cybertheft" in February , stealing nearly 4 million dollars of Ethereum, a type of cryptocurrency.

The lawsuit said that Salt never reported the original mod and the subsequent theft to external parties, including order forces.

The lawsuit said that Salt hired a law firm to investigate the original hack, so he stopped work before completing "for no apparent reason".

Salt's relationship with law firms is often of short duration, according to the lawsuit, which claims that the company has hired 25 companies separated from summer 2017.

The lawsuit also claims that the company's legal counsel is not authorized to exercise the law.

The co-founder now lives near Madagascar

Benjamin Yablon. (LinkedIn Headshot)

According to the lawsuit, in August 2017, Benjamin Yablon, co-founder and now president of Salt, moved to Mauritius, a small island nation off the coast of Madagascar.

Lechner and others questioned Yablon on the move and "it was said that it would be" beneficial "to Salt's loan platform from a tax perspective and that Mr. Yablon felt he could obtain additional auxiliary benefits from these government officials," he says. cause.

Later Lechner learned that Mauritius has no extradition treaty with the United States, in addition to the lax financial regulation, according to the lawsuit.

After moving to Mauritius, Yablon began to ask Lechner to approve large payments – $ 371,000 in one case – to other Mauritian residents, saying they would make "favorable presentations" to local officials, he says.

The lawsuit claims that Yablon accepted smaller payments for people after Lechner retired, but the other Salt executives began to exclude Lechner from important corporate decisions and information, and began paying less.

The lawsuit defines Yablon's actions as potential violations of the Foreign Practices Act, which prohibits bribery of government officials.

Salt & # 39; s Nealson has confirmed that Yablon lives in Mauritius, "where he and his team are pursuing our vision to expand our global offering".

CEO of another Denver company crypt mentioned

The case also raises questions about Erik Voorhees, founder and CEO of another Denver-based cryptocurrency company called ShapeShift.

Erik Voorhees, CEO of ShapeShift

"Mr. Voorhees has been identified by investors as a member of the Salt Board of Directors, which appears to be a violation of Mr. Voorhees's regulations with the SEC of 3 June 2014 concerning his unregistered offer of bitcoin-related securities" cause says.

"In the regulation, Voorhees agreed not to participate in any issue of securities in an unrecorded transaction in exchange for any virtual currency, including Bitcoin for a period of five years," the lawsuit says.

The role of Voorhees was highlighted in a story last week by the Wall Street Journal. In September, the paper published an investigation titled "How dirty money disappears in the black hole of cryptocurrency", which concluded that ShapeShift has processed millions of dollars in digital currencies belonging to criminal suspects.