[ad_1]

KB Management Research Institute 2020 Korea Single Person Report released

viewer

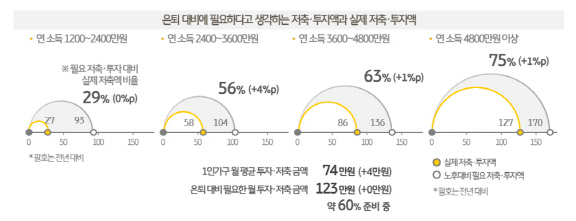

The estimated cost of retirement, estimated by 6 million single-member households, was 570 million won. For this, it is necessary to make investments and savings of 1.23 million won per month, but their investment and savings amount to only 60%. Also, in the case of single-person families with no intention of marrying, most of them have not considered how to deal with their property in detail.

According to the KB Financial Research Institute on the 9th, the actual investment and savings of single-person households were approximately 740,000 won. That’s about 60% of the monthly investment and 1.23 million won savings to raise 570 million won, which is the cost of retirement a single family thinks. The level of preparedness for pension funds varies greatly by income segment, and the low-income segment still lacks savings after covering basic living expenses.

The savings of single-member households, on the other hand, increased slightly compared to last year. Deposits and savings were the most common methods of preparing retirement funds. Compared to last year, more respondents said they were preparing with investment products and insurance, and it was found that most single-person households with fewer year-end liquidation deductions than multi-family households are preparing for retirement by receiving deductions from pension savings or IRP.

In the case of one-person families who are unwilling to marry, they replied that they will use their property as much as they want, rather than the inheritance, but many other cases have never thought of a specific method of property management.

The “lack of income” (37.8%) was cited as the most hindering factor in preparing for pension funds. It was followed by “no room after living expenses” (15.8%), debt repayment, and education expenses. By age group, more than half of the opinions that people in their 30s use them as much as possible and the opinion that “giving back to society” is higher than those between 20 and 40.

This year, the number of single-parent households in Korea is around 6.17 million, solidifying the position of the main family type. 12 out of 100 citizens live alone. The number of single-parent households in Korea is expected to increase by approximately 150,000 annually over the next five years, leading to an increase in the total number of households even after the point of population decline. By 2047, the proportion of single-person households is projected to exceed 30% in most regions of the country.

With respect to the financial assets of single-member households, the proportion of deposits and savings has decreased and the proportion of investing assets, deposits and withdrawals and cash has increased, reflecting the increased demand for liquidity-like assets and the recent increase in cash. Investment interest due to Corona 19. In addition, more than half of the financial products were used for cash without having to re-deposit after termination. Young people are more willing to invest in new stocks. Meanwhile, around 40% of survey respondents had loans, indicating that the percentage of borrowers has slightly decreased from the previous year.

On the other hand, KB Financial Research Institute housed 2,000 single-person families aged 25 to 59 residing in Seoul, Gyeonggi and six metropolitan cities and Sejong city (annual income of 12 million won or more, who make finance decisions on their own, live a single family for more than 3 months) This survey was conducted on the subject.

/ Reporter Lee Ji Yoon [email protected]

Source link