[ad_1]

The price of a family and house public announcement is 900 million, and in the case of a common name, over 600 million per person are taxed.

Even if you own part of the house … Excluding 20% of the capital, less than 300 million

Check your house taxes … You can request an objection within 90 days of receiving the notification

viewer

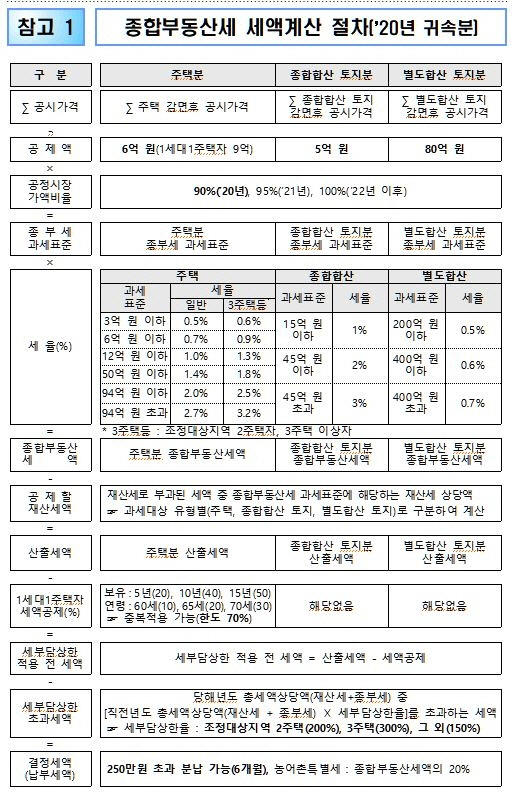

The recently announced global property tax for 2020 is only collected when the value of the taxable property exceeds a certain level after the first property tax has been collected. Each family is deducted 900 million won for a homeowner and 600 million won for co-ownership with a spouse or family.

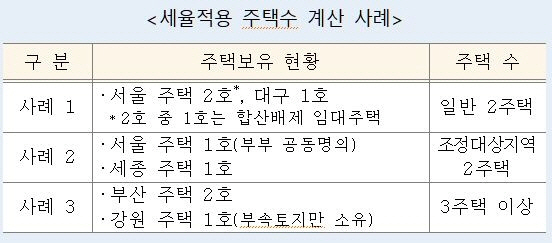

In principle, the number of houses is subject to property tax. It is the total number of homes subject to tax on the property owned by each taxpayer nationwide. Even if only part of the house is owned, it is considered to be the owner of a home and the number of houses is calculated when the tax rate is applied. You can check the taxable items at Hometax or at your local tax office. Below, we have summarized the questions and answers relating to the tax notification (report) and the payment of the final tax submitted by the National Tax Service.

viewer

viewer

– How taxation works.

△ Property tax is imposed firstly on the owner of the house or land by the municipality having jurisdiction over the location of the property and, secondly, if the sum of the taxable assets by type (housing, total / separate land) located nationally it exceeds the deduction for each type Decide and notify.

– The published price which is based on taxation is.

△ This is the price announced by the Minister of Land, Infrastructure and Transport and the head of a Si / Gun / Gu starting January 1st of each year. Standard buildings and single-family homes and standard land must be announced by the Minister of Land, Infrastructure and Transportation, and for other single-family homes and land, the head of the mayor, county or district having jurisdiction over the location of the real estate must disclose prices.

The published price for housing (community housing) is April and the published price for land is May. It can be found on the homepage of the Ministry of Territory, Infrastructure or the jurisdiction of the real estate area.

– What is the definition of a single family home?

△ When one of the family members only owns a home that is subject to property tax for housing, he is a resident under the Income Tax Act.

– If you own a home together with your spouse or family, the deductible is.

△ Each stakeholder is deducted by KRW 600 million. The deductible for a homeowner in the first family is 900 million won.

– How to calculate the number of houses when tax rates are applied.

△ This is the total number of homes subject to property tax owned nationwide for each taxpayer. Even if only part of the home is owned, the number of homes is calculated when applying the tax rate as it is considered owning a home. Excluded rental accommodations are excluded from the calculation of the number of accommodations when the tax rate is applied.

viewer

viewer

– Does it count the number of houses with inherited shares?

△ If the holding ratio is less than 20% and the published price equivalent to the holding fee is less than 300 million won, it is excluded from the number of houses when the tax rate is applied. However, when determining a house for a family, it is included in the number of houses and the published price for inherited houses subject to special provisions is also included in the tax base. In the case of multiple joint inheritance houses, it is judged on the basis of inheritance houses and all inherited houses that meet the requirements are excluded from the number of houses.

– The criteria for determining whether the region is subject to adjustment.

△ The determination of the location of the area subject to adjustment is based on 1 June of each year, the tax base date.

– How to check taxable housing and land specifications.

△ Hometax or Sontax (mobile hometax) You can search for taxable items and download the specifications using the “Search for taxable items” service. Taxpayers who are unable to use Hometax can receive a description of their assets after completing the identification process at the relevant tax office.

– In which cases do you report taxes

△ If the content of the notice differs from the facts or if the taxpayer wants to report it, he can report it and pay independently of the tax notice and the initially notified tax amount will be canceled. If you object to the content of the notice, you can file an objection within 90 days from the date of receipt of the notice, such as an objection or a request for trial.

– If you fail to notify the combined exclusion within the reporting period.

△ If you do not notify the combined exclusion within the reporting period (September 16-30), you can request an additional application during the tax payment period (December 1-15).

– If payment is not made by December 15th, the late payment penalty is.

△ If 3% late payment tax is imposed and the tax amount is more than 1 million won, 0.025% late payment tax is added every 1 day after the payment deadline has passed for 5 years.

– If you wrongly declare the tax amount, you will be penalized.

△ A penalty of 10% (40% for unfair underestimation) is applied on the lower declared tax amount.

– Among the tax services of Hometax, the elements that require access to an accredited certificate are:

△ A certificate is required for payment of taxes and requests for information on taxable items. It is not necessary for an installment application.

/ Reporter Jang Deok-jin [email protected]

Source link