[ad_1]

5 major banks open 6,700 per day

The actual burnout rate is only 38%

Application for “last car” before loan settlement

viewer

It was found that the number of new negative bank books rose to the highest in history before the “perpetual loan regulation” targeted at high-income workers. Compared to before the financial authorities announced the settlement, it has increased more than three times in ten days. It is interpreted as the result of the request to open a bank book before the application of the regulations, as the low interest rate and the rise in real estate and equity markets overlap.

According to the 29 banknotes, the number of recently opened negative bank books at KB Kookmin, Shinhan, Hana, Woori and NH Nonghyup Banks during the day was a total of 6,681 as of the 23rd. Compared to the 12th (1,931 cases), the day before financial authorities announced credit lending regulation on the 13th, it increased 3.5 times in about 10 days. A commercial bank official said: “According to internal bank statistics that can be compiled, the number of negative bank books set up on the last day is the highest ever recorded.”

Compared to the rapid increase in opening negative passbooks, the percentage of actual money withdrawn was not high. The negative bank book depletion rate (loan-to-limit ratio) of the four commercial banks averaged 38% on 26. On the bank’s side, it remained at the level of 32.6 ~ 43.5%, down compared to the same period last year. It means that the newly opened negative bank book has increased to the maximum ever, but the amount of money borrowed from this book has not increased that much. It is interpreted that the sentiment of “we do it” worked even if you did not intend to use a loan immediately prior to the settlement on the credit loan. A commercial bank employee said: “Clients who need immediate financing prefer loans with lower interest rates. It seems that the demand to open a passbook early in case of need in the future has increased.”

viewer

viewer

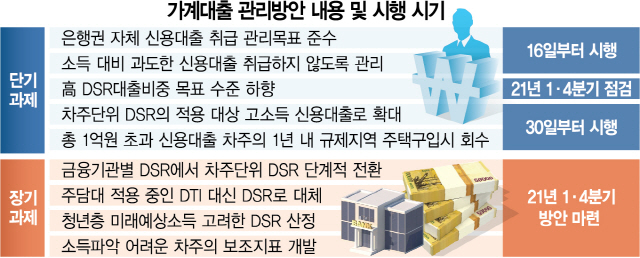

This “latest car demand” is driven by additional loan regulations, including loans starting from 30. According to the financial authority’s family loan management plan, starting from 30, for high-income earners with high income per annum of 80 million won or more, if the total credit loan amount exceeds 100 million won, a total debt repayment ratio (DSR) of 40% is applied. Until now, only when a mortgage loan was received as collateral for homes exceeding 900 million won in the regulated area, the 40% DSR was adjusted for each individual. If this regulation is applied individually, high-income people who already have a large amount of principal debit and credit loans, even if there is no principal debit or regulated home-based loan as collateral, cannot receive credit loans. additional. Also, if an individual who has received more than 100 million won in credit loans purchases a home in a regulated area within one year, the credit loan must be paid off within 14 days.

Anyone who had a credit loan exceeding 100 million won before the system was implemented and then simply extended or changed the interest rate and maturity conditions and renegotiated it is not subject to the regulation. In the case of negative bank books, once settlement is enforced, the contracted amount is calculated as the total amount of the credit loan, not the actual amount used. For this reason, it is an analysis that has focused on the request to obtain a loan in advance by the 30th of this month, which is the effective date.

In some cases, if the passbook’s negative burnout rate is too low, the limit can be reduced when the deadline is extended, so caution is needed. KB Kookmin Bank, for example, has put in place a system to reduce the loan limit based on the exhaustion rate for new or extended negative bank books with contractual amounts exceeding 20 million won since the end of July this year. year. If the average rate of exhaustion of the loan limit is less than 10% from the date of a new contract or extension of a negative bank book up to 3 months before the due date, the limit of the contract is reduced by 20% when it extends the period. Another commercial bank official also said: “Because the bank has the burden of accumulating provisions as much as the negative bank book limit, we are lowering the limit by consulting customers during the renewal process.”

/ Poor bird reporter [email protected]

Source link