[ad_1]

[ad_1]

What is it?

A public1, permanent2, append-only3distributed4ledger5.

What is that?

This story is part of our May / June 2018 issue

See the rest of the problem

subscribe

A mathematical structure for storing data in an almost impossible way to falsify. It can be used for all types of precious data.

Where does it come from?

"I worked on a completely new peer-to-peer electronic cash system, with no trusted third parties." These are the words of Satoshi Nakamoto, the mysterious creator of Bitcoin, in a message sent to a cryptographic mailing list program in October 2008. Including a link to a nine-page white paper describing a technology that some are now convinced to disrupt the financial system.

What is the blockchain for?

It is a new way of answering an old question: how can we create enough mutual trust to peacefully exchange something of value?

-

Reinforcement

Early civilizations used the threat of force as a reward for dealing in bad faith when it came to doing business.

-

institutions

The emergence of governments and banks provided central and organized authorities to which we could trust outsourcing, provided we trust them.

-

The network

The blockchains distributed over thousands of computers can mechanize trust, opening the door to new ways of organizing "decentralized" companies and institutions.

Nakamoto extracted the first bitcoins in January 2009 and with this came the era of cryptocurrency. But while its origin is obscure, the technology that made it possible, which we now call blockchain, did not create blue. Nakamoto has combined established cryptographic tools with methods derived from decades of computer research to allow a public network of participants who do not necessarily trust each other to agree, over and over again, that a shared ledger book reflects the truth. This makes it virtually impossible for someone to pass the same bitcoin twice, solving a problem that had hindered previous attempts to create digital money. And above all, it eliminates the need for a central authority to mediate electronic currency exchange.

Bitcoin's popularity began to grow rapidly in 2011, after a Gawker article exposed Silk Road, a Bitcoin-based online drug market. The imitators called "altcoin" began to emerge, often using Bitcoin's open source code. Within two years, the total value of the bitcoins in circulation exceeded $ 1 billion.

Soon, technologists understood that blockchains could be used to track other things besides money. In 2013, Vitalik Buterin, 19, proposed Ethereum, which records not only currency transactions, but also the status of computer programs called smart contracts. Launched in 2015, Ethereum – and now a series of competitors and imitators – promises to enable a new generation of applications that look and feel like today's web apps but are powered by decentralized cryptocurrency networks instead of a company's servers .

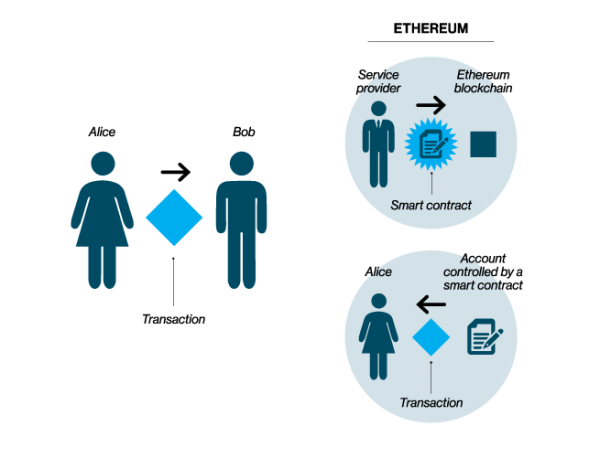

1. A transaction was born

In Bitcoin, one transaction is the transfer of cryptocurrency from one person (Alice) to another (Bob). In Ethereum, which includes an integrated programming language that can be used to automate transactions, there are several types. Alice can send cryptocurrency to Bob. Or someone can create a transaction that puts a line of code, called an intelligent contract, on the blockchain. Alice and Bob can then send money to an account controlled by this program, to activate it if certain conditions encoded in the contract are met. An intelligent contract can also send transactions to the blockchain in which it is embedded.

2. The transaction is transmitted to a peer-to-peer network

Let's say Alice wants to send money to Bob. To do so, Alice creates a transaction on her computer that must refer to a transaction passed on the blockchain in which she received sufficient funds, as well as her private key for the funds and Bob's address. This transaction is then sent to other computers, or "nodes", in the network. The nodes validate the transaction as long as it has followed the appropriate rules. Then the mining nodes (plus those of step 3) will accept it and become part of a new block.

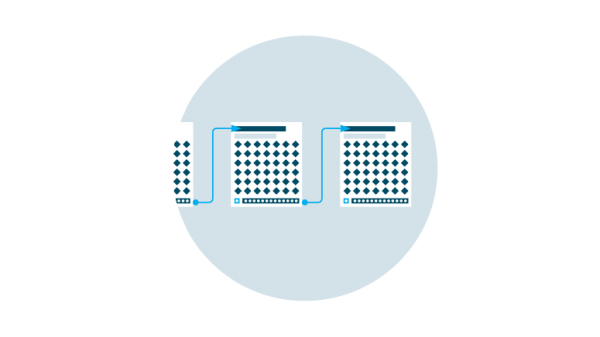

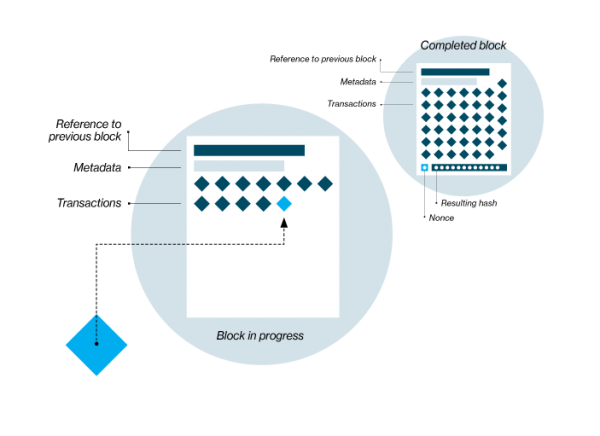

3. The rush to create new blocks

A subset of nodes, called miners, organizes valid transactions in lists called blocks. A block in progress contains a list of recent valid transactions and a cryptographic reference to the previous block. In blockchain systems like Bitcoin and Ethereum, miners run to complete new blocks, a process that requires the resolution of a laborious mathematical puzzle, which is unique to each new block. The first miner to solve the puzzle will earn some cryptocurrency as a reward. The mathematical puzzle involves randomly matching a number called nonce. The nonce is combined with the other data in the block to create an encrypted fingerprint, called a hash.

4. Completing a new block

The hash must fulfill certain conditions; if it does not, the miner tries another random nonce and calculates the hash again. It takes a huge number of attempts to find a valid hash. This process deters hackers by making it difficult to change the ledger. While some blockchain entities use other systems to protect their chains, this approach, called proof of labor, is the most tested in battle.

5. Adding a new block to the chain

This is the last step to protect the ledger. When a mining node becomes the first to solve the crypto-puzzle of a new block, it sends the block to the rest of the network for approval, earning the digital tokens in reward. The difficulty of extraction is codified in the blockchain protocol; Bitcoin and Ethereum are designed to make it increasingly difficult to solve a block over time. Since each block also contains a reference to the previous one, the blocks are mathematically concatenated. Tampering with a previous block would require repeating the job test for all subsequent blocks in the chain.