Blockchain is the subject of the moment in the supply chain. But what can you really do today for supply chains and where can you take us tomorrow?

Blockchain is "The New Internet", at least according to Accenture and DHL, in a recently published study on blockchain supply chain applications. "The implementation of the blockchain in logistics could eliminate the need for intermediaries, also verifying, recording and coordinating transactions in an autonomous way", notes the report. "Blockchain-based supply chains would eliminate an entire level of complexity from global supply chains."

Many are in agreement, including Jon-Amerin Vorabutra, senior vice president, risk, process and IT at Nova Molecular Technologies and former vice president of innovation at LoadDelivered Logistics. "This technology will allow for greater supply chain efficiency than in the past, from payments and audits to inventory and resource tracking," he says.

These big statements are just a small buzz around the blockchain and its application to the supply chain. But what is the reality of adoption rates today? Can blockchain really offer all the benefits that you claim to offer? And is it a technology for every size and type of company?

The short answer to these questions: it depends. The longest answer deserves to be explored.

But first, some background.

What is blockchain in the supply chain? Simply defined, blockchain is a distributed database that contains records of data or digital events in a way that makes them resistant to tampering. It is essentially a secure "single version of truth" about transactions and activities that take place through complex supply chain ecosystems.

While blockchain participants can access, inspect or add to data, they can not modify or delete existing data. The original information remains, leaving a trace of public and permanent transactions. Depending on the type of blockchain, data privacy protection can be very robust, as well as functionality for end-to-end visibility, monitoring and traceability, security and condition monitoring.

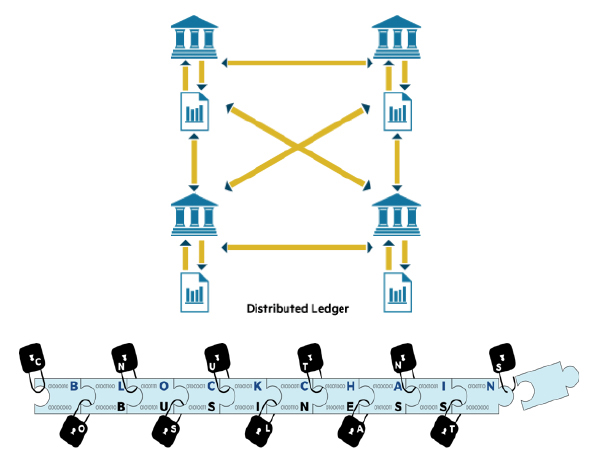

"In the end," says Drew Miller, CEO of Blockchain Business Consultants, "blockchain is a record-keeping mechanism that makes it easier, safer and easier for companies to work together on the Internet." (See Figure 1.)

Figure 1: Blockchain supply chain distributed with a single accounting platform

Source: Drew Miller, 2018

Blockchains are available in two versions: private and public .

In a private blockchain, a & rsquo; private entity (i) – Walmart or Amazon, for example – controls the computers and the blockchain. Admission is by invitation only of business partners such as suppliers, buyers, transport companies and financial institutions. All parties agree to participate in the rules of the private blockchain.

"The authorized private blockchain allows companies to start extracting commercial value from blockchain implementations," writes McKinsey & Company in a 2018 report titled Blockchain Beyond the Hype: What Is the Strategic Business Value?

"Dominant players can maintain their positions as central authorities or join forces with other players in the industry to gain and share value," says McKinsey. "Participants can gain the value of secure data sharing by automating the control of what is shared, with whom and when."

Unlike an authorized private blockchain, a public blockchain is completely open. Anyone can participate and participate. Bitcoin, the world's first cryptocurrency (e-money), was one of the first public blockchain networks.

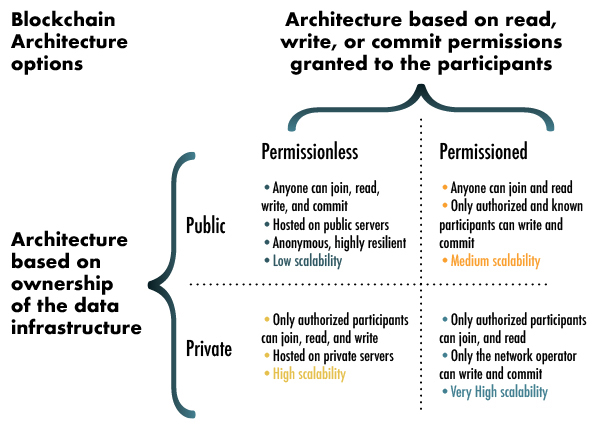

Public blockchains have two significant disadvantages for commercial users. One is the significant amount of computational power required to keep a register distributed on such a large scale. Two are the lack of privacy and protection of proprietary data. Figure 2 illustrates the architecture and public private blockchain functionalities

Figure 2: Private and public blockchain attributes

SOURCE: McKinsey & Company

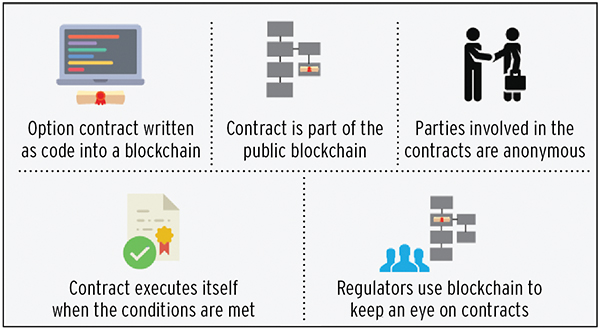

Smart Contracts: the key enabler [19659026] Having a distributed blockchain log is okay, but what really makes this technology pay off is built-in smart contracts. "Smart contracts are just as important as blockchain," says Miller. "Put your contract terms on the blockchain and the platform will execute these terms as soon as you receive confirmation that the activities have been completed and comply with the terms of the contract."

For example, if a truck delivers a shipment and meets the contractual service – level agreement, the smart contract automatically issues the payment. No waiting for payment, no invoicing, no administrative costs. (See Figure 3.)

Figure 3: Operation of Smart Contracts

Source: Codebrahma, 2018

How far is the widespread adoption of blockchain in the supply chain? Most experts say three to five years. "But that timing could accelerate if a large and" neutral "company, like Google or IBM, launches an end-to-end commercial blockchain," notes Steve Banker, Vice President, SCM at ARC Advisory Group. At that point, adoption could increase rapidly.

The key difference in this scenario is that the "owner" of the blockchain is a neutral party, and not a Walmart, for example, where companies could worry about the security of their property, competitive information.

Another essential element for widespread adoption: the blockchain must cover the end-to-end supply chain, not just point-to-point transactions. It needs to cover every single "touch" in the supply chain to achieve maximum return on investment and make the change management process worth the effort and cost.

Blockchain is right for you?

Blockchain, at its current level of maturity, is not right for every type and size of company.

"For large companies, carriers, third-party logistics service providers (3PLs) and shippers, I see an immediate value," says David Broering, president of North American Non-Asset at the NFI. "The international supply chains have all kinds of moving parts and many actors: transporters, ports, manufacturers, suppliers, financial institutions, government authorities and customs, so having a safe and shared control of these moving parts is absolutely logical. " [19659005] Blockchain also makes sense for the high-value and / or heavily regulated cold chain sectors such as food and pharmaceuticals, Broering says.

From a trucking perspective, however, Broering says that investing in blockchain is not a viable strategy at the moment. He cites several reasons:

- The average length of the raid is short – only 700 miles – a simple point-to-point transaction.

- The accomplishments to the trading partners are limited in the number-shipper receiver. [19659039] Trucking companies typically do not have profit margins that allow investments in always-on connectivity or big data systems, including blockchain.

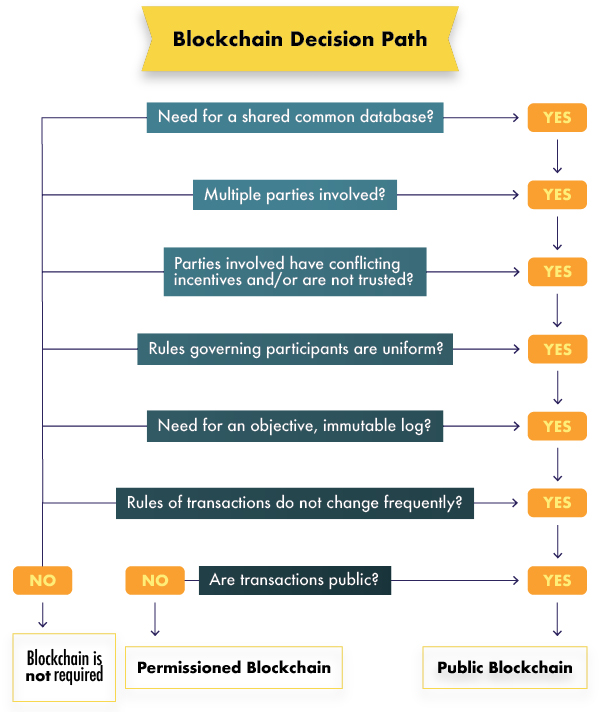

To make an informed decision on whether or not to implement blockchain, Miller recommends the use of a decision matrix (Figure 4). Instead of simply answering questions or answers, it suggests weighing responses on a scale of 1 to 10, where 1 is "not important" and 10 is "critical". Then calculate the score to see where the answer falls on your decision scale.

Figure 4: Making an informed decision on the implementation of the blockchain

Evolution, Not Revolution

Blockchain is a technological platform that here remains and holds great potential for the 39; supply chain environment.

Having said that, widespread adoption remains years away. The first to adopt will be those companies and sectors that have the highest value (diamonds), high risk (defense technology), high compliance requirements (fresh food and controlled temperature) and high service performance requirements (3PL that serve them a -stake customers).

Return on investment is a problem. Adopting blockchain means restructuring the way supply chains operate. Therefore, change management, both internal and external, is an important business and involves a significant cost.

Balancing the cost of change over performance in terms of efficiency, speed and agility, risk reduction, and ultimately, profitability is something that every business will have to assess regularly as technology evolves rapidly.