[ad_1]

[ad_1]

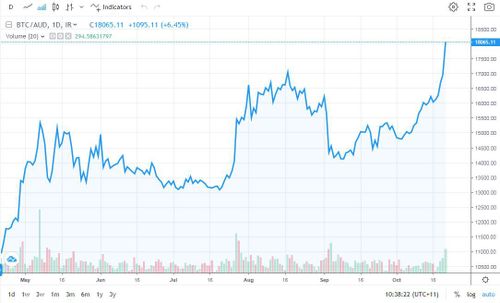

Bitcoin is booming again.

Overnight, the now infamous cryptocurrency hit a high of A $ 18,267 for one Bitcoin, following the announcement that the PayPal money transfer service would allow its users to trade using virtual currency.

Using the currency just like any other forex, PayPal’s 26 million merchants will begin accepting Bitcoin as payment for goods as early as February 2021.

It’s another arrow forward for Bitcoin, which had considerable success during the COVID-19 pandemic as investors look to currencies that aren’t aligned with any national power.

In March, the cryptocurrency was trading as low as $ 8736 per coin, meaning that in just seven months, it has added around 110% of the value.

The total market is now worth $ 337.1 billion.

For context, Bitcoin’s highest price ever reached was $ 25,037 on December 11, 2017, during the “bubble boom” which saw early adopters gain widespread notoriety for trading their Bitcoins for Lamborghini, owned high-end and fame.

Nigel Green, chief executive of the deVere group and advocate for cryptocurrency, said Bitcoin is growing in legitimacy every day.

“Incredibly, there are still some financial ‘experts’ and financial watchdogs who believe cryptocurrencies are not the future of money,” Green said.

“The decision by one of the world’s largest payment companies to allow customers to buy, sell and hold Bitcoin is another example that exposes Bitcoin deniers and cryptocurrency cynics as being on the wrong side of history.

“Let’s be clear: this is an important step towards the mass adoption of digital currencies.”

“Part of the evolution of cryptocurrencies over the past few years has been an attempt to address some of the major shortcomings that have prevented Bitcoin from functioning as money,” wrote researchers from the RBA’s payments division.

“However, it remains the case that no cryptocurrency currently functions as money in Australia or as a widely used payment method.”

Explained in five minutes: what is Bitcoin?

1. Bitcoin is a form of online cryptocurrency that allows you to transfer money electronically. It is decentralized, which means that no one regulates or controls it except for market demand.

2. It was created by a group (or a single person) of programmers under the pseudonym “Satoshi Nakamoto” in 2009.

3. Bitcoins are “mined” by computers that solve incredibly complex mathematical equations. Like coal or oil, there is a limited number of Bitcoins available to mine, estimated at around 21 million.

4. You cannot mine Bitcoin on your home computer, it requires specialized programs and hardware which have increased the difficulty of mining a Bitcoin.

5. Bitcoin underwent a dramatic explosion in value in late 2017, before suffering one of the most catastrophic falls in value in the currency ever.